Most small businesses we know have made zero to minimal revenues since the lockdown started on March 15. But that has not stopped our obligations to pay rent, wages, utilities, and amounts owing to suppliers. Fortunately, the government is rolling out its plan to gradually reopen the economy. I emphasize gradual because the experts anticipate a vaccine in 18 to 24 months. So normal as we know it, and by extension, the revenue we have grown accustomed to, will likely not return until then. Which leads us to today’s question: How do I manage with less money?

Creating a bridge to the vaccine

There are government assistance programs. But relying on government programs may not be sustainable and will likely start to wind down soon. So, the onus will be on you to build that bridge for your business to the point where a vaccine is rolled out. And a robust cash management process is the best place to start. A proper cash management process, in a nutshell, will allow you to take the necessary actions to manage your cash situation, not just at this point in time, but over the next 18 to 24 months, when it’s very likely that you will have less revenue to work with.

Your 3 sources of cash generation

There are 3 sources and opportunities from which your business generates cashflow:

- Operating Activities – Cash from day to day transactions, such as receipts from customers, and payments to suppliers, landlord, employees, municipalities, etc. These activities are represented by the Working Capital in your balance sheet.

- Investing Activities – Cash receipts or payouts from disposals or purchases of assets to support the productive capacity of the business, e.g., buildings, cars, trucks, machinery, computers, etc.

- Financing Activities – Cash receipts or payouts related to bank loans or line of credits, shareholders equity or soft loans from family or friends.

Taking a holistic view of these 3 sources during your planning will enable you to better utilize all sources of cash at your disposal to overcome any shortfall you are experiencing at a point in time. And doing a projection of your cash flow into the future allows for timely actions to tackle cashflow fluctuations within your control.

Tried and proven strategies to tackle cashflow fluctuations within your control:

A. Shorten your cash conversion cycle

Your best strategy over the next 18 – 24 months starts with an asserted effort to improve your working capital efficiencies or try to increase cash from your Operating Activities. You will achieve this by shortening your cash conversion cycle. Example: you could arrange to pay creditors 15 days later, try for a leaner, just-in-time (JIT) approach to inventory management and be more assertive in collecting from customers, e.g. introducing email deposits.

B. Improve your working capital resiliency

Further opportunities to increase your cash from operating activities and shore up your working capital will come from these (and other) additional actions:

- Sales – You may employ social media, curbside pickup, delivery, and other innovative promotional campaigns to improve sales. This will lead to a positive impact on cash inflow, especially in the latter 12 of the 24 months projection, when consumer confidence starts to improve.

- Rent – You may use the opportunity to start or continue dialogue with your landlord to arrange rent reduction or deferral. Your negotiating strength is that your landlord needs to have the space occupied.

- Wages – You should seek to retain enough employees to meet the anticipated operating capacity.

- Interest payouts – You should reach out to your banks to try reducing interest on loans and credit cards. Banks understand the challenges business owners face and are being prodded by the government to be flexible.

C. Use cash from investing activities to cover shortfalls from your operating activities

You may sell an equipment or vehicle that is no longer required to provide cash to cover rent payments and wages for 2 periods. This could buy you time, while customers / revenues continue to return.

D. Use cash from financing activities to cover shortfalls from your operating activities

You may tap into existing line of credits, bank, or family loans to provide a needed cash float, while inflows from revenues are low.

Government assistance and guidelines

Including the current government assistance and adherence to Covid-19 health guidelines may have the following impact on your cashflow planning:

Operating activities

Cash inflows may arise from the following government programs:

Rent

A 75% reduction over 3 months via the Canada Emergency Commercial Rent Assistance (CECRA), if eligible and if you win the landlord’s buy-in.

Wages

A 75% 3-month (to be extended) subsidy via the Canada Emergency Wage Subsidy (CEWS), if eligible.

Tax and customs duty

A 2-month and 3-month extension of remittances of income tax and GST/HST & customs duty to the Canada Revenue Agency (CRA).

Investing activities

You can anticipate a cash outflow because of the need to adhere to the health guidelines to limit the spread of the virus. This include measures to ensure physical distancing, and one or all of; signage, installing Plexiglas barriers, increasing air flow and proper sanitation practices, and providing personal protective equipment.

Financing activities

Cash inflow may arise from the $40,000 interest-free loans through the Canada Emergency Business Account (CEBA) or the Regional Relief and Recovery Fund (RRRF), if eligible. With a further inflow of up to $10,000 from debt forgiveness, if the balance is repaid on or before December 31, 2022. The RRRF do offer another option where inflows between $50,000 and $500,000 may be accessed.

Spreadsheet or accounting software

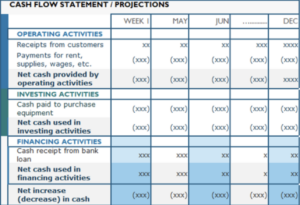

I recommend you use a spreadsheet or accounting software to complete your plan. It should, as illustrated in fig.1 below, comprise a daily, weekly, or monthly forecast of your best estimate of anticipated cash inflows and outflows from operating, investing, and financing activities. Which when combined, sums to your net cashflow position at end of day, end of week, month, or period.

Fig. 1

Your actual results should be similarly recorded and compared to your estimates, analyzed, and tracked at least weekly in the first 12 months and monthly thereafter if economic conditions improve.

Need for bootstrapping

These unprecedented times will require you “thinking outside the box” to ensure your survival.

You may consider deferring your personal mortgage through the 6-month Mortgage Payment Deferral program. This, though not a direct business cash flow, will reduce your personal cash outflow, and lessen your reliance on the business.

You may apply for the Canada Emergency Response Benefits (CERB), if the business is earning less than $1,000 per month as a direct consequence of Covid-19 related reduced sales. This has the same effect of the above mortgage deferral, of relieving your stress and anxiety from relying solely on the business for your livelihood.

Also, approaching family members and / or friends for soft loans may be considered. Some may have suffered a relatively softer financial blow and may be more than willing to help you ride out the storm.

Pivot, pivot, pivot!!!!!!

Lobby, lobby, lobby!!!!

It is likely that the business will have a negative cash position from its combined operating, investing, and financing activities throughout the next 18 – 24 months. The silver lining here though, is that by doing the projections and tracking to actual, you have a more informed position of your situation and can take appropriate action in a timely manner.

An equally important opportunity for completing the projection and tracking to actual is that it provides you and your lobby groups, like the Canadian Federation of Independent Business (CFIB) and the Canadian Black Chamber of Commerce (CBCC), tangible evidence to make timely requests for additional government assistance for business owners. This will likely lead to more proactive government actions compared to the current reactive untimely responses.

Conclusion

There is no one-size fits all solution here, but I strongly believe that creating a 24-month plan underpinned by a robust cash budget process will go a far way to restore your business resiliency and preparedness to grow following the roll out of a vaccine.

To learn more about how our Business Solutions may positively impact you maintaining your business viability and restore its value, you may connect with me for a FREE 30-minute no obligation consultation.

Effectuation Optimum develops these and other management strategies for business owners to help them effectively manage their affairs. Business owners who opt to partner with a professional will position themselves to systematically overcome and grow from these challenging times.